Who hasn’t heard of it, yet? The price of copper, together with the respective miners, can only see one way: up, up and upper! This thesis is based on the ongoing electrification of our society. Where there is electricity, copper is needed. More electricity demand = more copper demand, right? What sounds plausible, has some weak points to it. Actually, I am even skeptical that this will play out in the way that the majority thinks, at the very least in the short to medium term.

Summary and key takeaways from today’s Weekly

– The reporting about copper is very one-sided, calling for higher copper prices due to demand massively outpacing supply being already a foregone conclusion.

– The only thing that’s safe is that supply will grow by c. 20% – what if demand disappoints?

– There a good reasons for this currently unpopular thesis.

I have some serious doubts that copper is the proclaimed “safe bet”.

Coming straight to the point: I just don’t see the running electrification as a one way walk in the park which will only consume more copper that cannot be produced fast enough, resulting in straight up higher copper prices and the respective customers overbidding themselves just to get a hand on the crucial metal, no matter the price.

The thesis sounds pretty logic at first sight, though.

More BEVs, more and stronger electrical grids, more heat pumps and air conditioners as well as of course more windmills and solar panels. This seems to be set in stone.

I go along with the supply side of things. These plans should be tough to realize as there’s seemingly not enough copper. Accordingly and with ever lower grades of copper in the mines, the effort to bring new copper supply up becomes higher, likely making copper more expensive.

As my readers know, I prefer to look at the supply side because it is slow-moving and (relatively) better predictable than the more shaky demand side.

What I have serious problems with is that the whole copper story is not really questioned. The truth is, in order to have higher copper prices on a sustainable basis, there must be at least a reliable demand situation. But what if it completely collapses?

This is what I am going to question in this Weekly on a broader basis.

Will it happen as the majority thinks or not?

I don’t know whether I will be right. This is not the point. What I want to achieve with today’s episode is to question certain narratives and to put the risk side into the spotlight. Where I start to feel uncomfortable is when only chances are discussed. But what if you’re wrong? What could happen in the worst case?

These thoughts and questions are part of every analysis I am conducting.

Usually, the majority is wrong! And there are good reasons that the copper thesis will be tested, possibly with a surprising outcome for many.

What I don’t like is a too high insecurity. And this is the reason why I haven’t bought the copper story, yet. It is also one of the reasons why I haven’t published any research report about a public copper company. The other reason is, I’d like to find a producer outside of Chile, Peru or Africa with great economics.

So far, I couldn’t find any available one.

To make it worse, two companies which had the potential for an appearance in one of my research reports, have been already acquired. In one, I was simply too late, already as I discovered it. The other was scooped up while I was doing the research and waiting for the next earnings announcement.

Today, I am going to discuss the supply side of copper where I go along with the broader consensus. But then, I will present some facts that could alter the whole copper-is-only-going-up thesis.

Since I have started this blog and my memberships, the average total return of my closed ideas is +19.6%, comfortably beating the S&P500 and the iShares MSCI World ETF.

I am also ahead “live”, looking at all my active and closed ideas. My so far published 15 ideas on average performed by +11.0%, while the S&P500 is lagging with just +8.5%. The iShares MSCI World ETF is even further behind with only +7.4%.

Beating the market is clearly possible!

If you struggle to find high-quality investment ideas that are not already “priced for perfection”, consider becoming a Premium or Premium PLUS Member, to receive my exclusive research reports with my best and market-beating stock ideas.

The supply side

As I am not writing here anything ground-breakingly new, this section should be rather viewed as a sum-up of what others already have discussed in-depth. But it’s necessary to be aware of as the introductory part to what follows next when I start to question certain narratives and foregone conclusions.

Starting from a bird’s eye view, where does copper come from?

One of the reasons I had difficulties in finding a suitable copper stock was that most companies have significant operations either in Latin America, namely Chile and / or Peru as well as the D.R. of Congo. Or you find certain huge projects like Grasberg in Indonesia which are clearly not tier 1 jurisdictions.

And this is where the majority of copper comes from, but also where the majority of reserves are hidden, as the following charts show.

Note: As I don’t have a paid account, I took the anonymized charts of Statista and wrote in the names of the respective countries myself, using data from the other linked sources. Not perfect, but a suitable enough broad-brush approach.

First, copper production of 2022:

Then, estimated copper reserves per 2022:

And here an alternative to the last chart showing the reserves in relative terms, however, not including Mongolia and being a year older:

Not spending too much time on these charts, the key points are:

- Chile and Peru are the two most important countries, regarding production and reserves, although it could change with time

- there are a few countries with high reserves, with currently no significant production like Mongolia (going to change over the next years)

- Australia is the most important “Western” country

- the USA is on both charts, but its production as is is too low to even supply itself with enough copper

- surprisingly, Canada is completely missing – usually a frequent name when it comes to commodities, but not regarding copper

Bottom line here, the reliance on rather politically fragile countries – especially Peru and Chile in the not too distant past – is very high.

This is why I was trying to find a pure-play Australian or Canadian copper miner for my members. Unfortunately:

- Australian copper miner Oz Minerals received a bid from BHP (ISIN: AU000000BHP4, Ticker: BHP)

- Canadian copper miner Copper Mountain Mining received a bid from Hudbay Minerals (ISIN: CA4436281022, Ticker: HBM)

There’s another pure-play Australian copper miner (relatively small and volatile, hence I am not giving its name) with way above average copper grades and reserves of at least 10+ years which I am watching.

Unfortunately, it suffered from massive rain falls in March which forced the company to stop operations at one of its two mines. With its half-year results, it now announced a hefty capital raise, causing a dilution of 40%…

Of course, copper could spike due to political or civil unrest in certain countries – but this is not what I base my investment thesis on.

Equally important is to have a look at some production numbers.

Just to throw in some ballpark numbers for a first orientation, here is a chart from the International Energy Agency, predicting the required supply of copper in two scenarios:

The first, let’s call it the base case, sees an increase of copper supply from mining (light blue columns) by some +20% until 2030 (from c. 20 Mt to 24 Mt) with only little more after that towards 2040. The second case is more optimistic, but to spot an interesting supply-demand imbalance, let’s assume that the base case with its lower supply will be closer to reality.

Total current supply (light and dark blue combined) from mining and recycling, is around 24 Mt. Until 2030, close to 30 Mt shall be required per the above digram.

The Wall Street Journal, citing consulting company McKinsey, threw around similar numbers, namely 30.1 Mt of available supply in 2030 that will be facing demand of 36.6 Mt for the ongoing electrification.

Let’s just take these numbers at face value.

The result would be a gigantic deficit of 6.5 Mt. or more than 20% of supply.

Please note, higher supply is almost sure, as miners are investing.

In brief, what many sources are saying is: Supply will rise, but demand will rise faster.

Until here, let’s just assume that copper demand is going to rise massively (which I am going to question a bit in the next section), requiring higher supply.

This means, new supply must be found and production obviously increased.

Especially, if you see pictures like these:

After more than 70 years of increasing copper output, Chile seems to have hit the ceiling. One of the big reasons is that copper concentration (also called “grade”) is declining, requiring more rock to be moved for the same amount of copper.

Which self-explanatory increases production costs.

If you look closer, you will notice that the peak was already prior to 2020, indicating that some serious issues have already been longer in the making. Add to this that the last CEO of the world’s biggest copper producer, state-owned Codelco (Chile), left after less than a year (see here), exactly due to these issues for private reasons.

Declining copper grades – a serious issue – are not a thing that suddenly occurred:

In 2022, Codelco reached a fresh-new ten-year low in copper grades! As said, this is the world’s biggest copper producer.

To put it into perspective, grades around 1% today are already called great, while it was common decades ago to find sources with 3% or more.

In their half-year report on p. 5 and 6, you can see that overall copper production declined by 13%, comparing half year 2023 to HY 22 (see here). Further, it should be not that surprising that Codelco lowered its forecast for the whole year, calling out lower volumes and higher costs per pound.

At current levels, Codelco’s copper production is running at a quarter-century low!

John Polomny, a YouTube channel I can highly recommend, summed it up nicely on one chart:

Little surprising, urgently needed supply must come from somewhere else.

At the same time, the US is doing things like these:

Also, a project in Arizona was blocked (see here).

Energy transition – yes, please – but digging the minerals – no, thanks. Let others do the work?

To quote Robert Friedland, a mining billionaire and one of the most famous faces due having discovered two gigantic copper complexes in Mongolia and the D.R. Congo:

“Mongolia was an adventurous location. So was the Democratic Republic of Congo. But this has to be done. Absent this effort, there is absolutely no chance of an energy transition. It’s a fantasy.”

Robert Friedland, article of Mining.com (see here)

So, over the next years the powers should shift noticeably, towards even more exotic locations like Mongolia, Indonesia and the D.R. Congo.

Mongolia with the Oyu Tolgoi mine (owners: Rio Tinto (ISIN: GB0007188757, Ticker: RIO) and the Mongolian government) is one of the key projects. But also the Kamoa-Kakula mine in D.R. Congo, where Friedland’s company, Ivanhoe Mines (ISIN: CA46579R1047, Ticker: IVN) has a significant stake in.

If you want more background information about the supply sitution, I recommend you to read this article from Mining.com (see here). There, they show among others the following chart, where you can see Oyu Tolgoi more than tripling and the Kamoa-Kakula mine in D.R. Congo to double their respective production until 2027.

In other sources it is assumed that Kamoa-Kakula will become even the world’s second biggest mine in the 2030’s.

I’d like to close this section with a quote from the Mining.com article, referring to the Mongolian mine in their introductory part of the article (highlights by me):

As demand for copper surges, supply is increasingly likely to come from mines like this one on the arid steppe: expensive, technically complex, outside traditional copper jurisdictions and operating under the eye of governments jealously guarding their natural resources.

Mining.com (see here)

Two comments from me:

- Why should local governments give away their precious resources for free?

- And the other: they are assuming that demand will be massively up.

As written above, the basic assumption is that copper supply will rise, but not fast enough to catch the skyrocketing demand.

We could talk longer about the seemingly distressed supply side of copper. But what if demand does not come in as high as predicted while supply will be up by say 20%? Bull markets in commodities occur when there is a shortage in supply, not when supply is growing!

I can tell you one thing:

If you rely on higher demand in a market where supply is increasing, too – you are close to burning your fingers.

Let’s risk a look into that direction.

The demand side – where I’m seeing issues

A key statement of the whole story is that the copper market is “tight” and it is only getting more extreme the further we go.

To kick off this section and to show you what the common expectation is, here is a quote from the WSJ article above (highlights by me):

“The market overall is pretty tight. Longer term there’s a narrative around resource scarcity and the green transition with EVs and renewables as well as the build-out of electricity grids. On paper it’s quite a substantial supply gap opening up over the next 10 years.”

Robert Edwards, copper analyst at CRU, quote from WSJ article (see here)

Increasing supply is masqueraded as a shortage due to even higher demand. Or in other words, there is no plan b presented, should demand come in lower than expected.

It goes even crazier as another analyst is cited to have said that copper demand growth is even “locked-in”. Everyone is sure that it is only a question of when, not if, the green transition will require way more copper than will be available.

Further, in the WSJ article it is written that in 2020 only 4% of copper was consumed for “green uses”. Until 2030, the demand shall be so extraordinarily high that 17% are said to be needed (on a then higher supply base, effectively more than quintupling).

All in all, copper supply must be 54% higher to meet demand goals.

I don’t know about you, but my stomach starts to turn around when I read such sentences.

What really makes me feel uncomfortable is that this copper building / story is constructed on higher demand, instead of too low supply.

I’d prefer a situation like in silver, coal or oil – topics that I have already written about. There, you don’t need higher demand, because supply already now is pressured due to underinvestments. In copper, however, massive investments are being made.

But what if something happens that is not being talked about?

What if copper demand does not reach the amounts that are being predicted? What if it even misses massively?

Unlikely to happen? Brace yourself for some breath-taking developments.

While it is clear that only silver has better conductivity capabilities than copper, it is way more expensive – too expensive to be used on a broader scale. Currently, silver costs around a whopping 103x more than copper on an equally weighted basis (silver is priced in ounces, copper in pounds – the conversion factor is 16x ounces = 1 pound).

This way, silver is no practicable alternative.

But three other things are possible and not even unlikely, lowering copper demand, with the power to sabotage the “safe copper bet”:

- technological advancements

- copper being partly replaced by aluminum which also has great conductive capabilities, at the same time being lighter by weight and cheaper

- a failure of “Energiewende” and the “green transition” (but, psst…)

Regarding the first point, first advancements have already been achieved in electric vehicles, as for example Tesla – wich unfortunately is not credited enough for its technological achievements, but bashed for burning batteries – announced in May, referring to its soon to be available Semi-Truck the following.

Elon Musk said:

“First approximation, that means we need only about a quarter as much copper in the car as would be needed for a 12V battery, so that’s a big deal because people often worry about whether there is enough copper. Yes, there is.”

Elon Musk, (see here)

A cut of three quarters does not seem like nothing to worry about, does it?

In other words and certainly a bigger leap forward until realized, but this means that 4x more BEVs could be produced, using the same amount of copper! And BEVs are a key pillar of the “green transition” – see the chart below. Under these circumstances, BEVs would need to increase by a factor of at least 8x (4x due to copper savings and another double to hit the predicted double in demand).

I have first doubts.

Point two aluminum.

In this must-read article from mining.com (see here), the authors are citing an analysis by BMO Capital Markets. They write that there is already industry activity in trying to at least partly, at times even to completely substitute copper.

Not mincing words, they are massively shaking up the whole copper investment thesis.

Just in their base case, BMO sees a potential of 10 Mt of copper demand being eliminated – by 2030. Just to remind you:

- currently, demand is somewhere between 20–25 Mt

- demand is seen by most pundits to reach 36.6 Mt in 2030

- subtracting 10 Mt, results in 27 Mt

- supply is forecasted to be around 30 Mt

And suddenly, we could have a copper oversupply of more than 10%!

“Such ‘fear substitution’ would be a challenge to the longer-term demand thematic and would have the potential to significantly hurt both industry volumes and prices.”

Mining.com (see here)

The affected areas are electricity transmission, distribution networks, communication cables, renewable energy generation as well as even air conditioning or the transportation sector.

Wait: Aren’t these all also key pillars of the “green transition”?

But what’s the rationale behind aluminum (see here)? Well, aluminum has only c. 60% of the conductivity capabilities of copper, that’s a given.

Advantages of aluminum, however, are:

- its abundance, being the third most abundant element in the earth’s crust

- it is 100% recyclable, already melting at 660°C (copper: 1080°C) , i.e. it is easier and with less energy consumption separable from other stuff

- it weighs only less than a third compared to copper

- it costs just about a quarter to 30% currently

(aluminum is priced in USD / t, copper in USD / pound, resulting in a conversion ratio of 2,200, meaning aluminum costs a buck per pound only while copper is traded for c. 3.75 USD)

While it is unlikely that copper will be completely substituted by aluminum, as its clear conductivity advantages are needed here and there, what speaks against using aluminum in lower-quality products or where weight is of greater importance?

Why should small city cars that only drive slowly without fast acceleration not use aluminum and at the same time save some weight (increasing range)?

Or air conditioners?

Which leads us to point number three – energy producers.

What about too high costs and uncompetitiveness? Not possible? Let’s have a look at some “green energy” heavyweights commenting:

In order not to be suspected of cherry-picking just one convenient example, here’s another one that has sent a blast through the industry:

To recap and put the finger even more in the wound, Ørsted (ISIN: DK0060094928, Ticker: ORSTED), just like Vestas Wind Systems (ISIN: DK0061539921, VWS) have been both posterchildren of “successful green energy”.

They were so successful, that Denmark – a country not necessarily known for being pro-nuclear, but heavily pro-wind as you can think of – has started a debate about the introduction of nuclear energy.

What if I tell you that they (not only Ørsted, but in fact the whole wind industry) are already having problem, even without the price of copper having shot up?

In the case of Ørsted, an ever growing debt load, together with now high interest rates are a serious threat to them.

But where they really excel it to beg for taxpayer’s money to bail them out for their uncompetitive business and gambling with high debt.

Here’s what the CEO had to say in the latest earnings call:

I think it is not necessary to mention that Ørsted has never generated any meaningful positive free cash flow over the last decade, while patting itself on the back for great returns?

They did not even manage to increase their operating income (before interest expenses), while sales grew.

Just look at the chart of Ørsted – is this a success story with being down by some 70% from the top? Markets don’t lie!

These are my three main points.

But they are only “inside” the transition.

“Outside”, you should be aware that China in general and China’s property (Evergrande, Country Garden, anyone?) sector specifically has been responsible for a big chunk of copper demand in the last twenty years.

Depending on where you look (e.g. here), you will find numbers like

- “50% of world’s copper demand comes from China”

- and that “25% of China’s GDP comes from the property sector

The current economic slowdown in China should rebalance – in a negative way – any higher copper demand (assuming I am completely wrong with the above). It is debatable, whether this is not even an overly optimistic guess.

But I am not finished, yet.

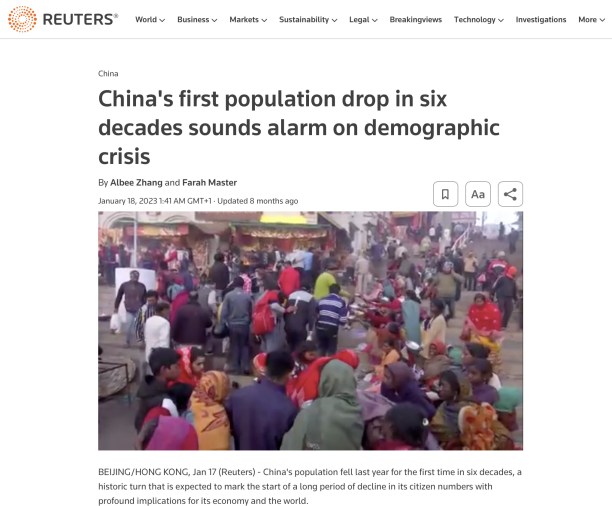

China, not being known as an immigration country, in early 2023 rang the alarm bell with the following piece of news:

I lack the creative imagination to see how this shall support copper prices, even further assuming there won’t be any demand drop for copper from other struggling economic areas.

Basically, the idea of investing at a favorable risk-reward ratio means that you place your bet when there is a high enough margin of safety, i.e. when there are currently doubts and weak belief. To the contrary, one should be cautious when a possible future development is already a foregone conclusion, the more so if it is politically motivated and subsidized.

Bottom line here, it does not look good under the hood.

Instead of copper, I prefer silver. Silver is a market where a shortage already exists. You don’t have to rely on exploding demand to be right. Plus, most miners are struggling to replace their reserves while being handicapped by brutally higher production costs.

Last week, my Premium and Premium PLUS members received my best stock idea to play this market. I presented my members a company that generates massive free cash flows in the current environment due to having favorable economics and ultra-low production costs.

It uses its free cash flow for exploration projects as well as for a first buyback. Silver miners are not known for buying back stock! The balance sheet is debt free.

I think it is also the most attractive takeover target, but management won’t give this jewel away for peanuts, that’s for sure!

Conclusion

The reporting about copper is very one-sided, calling for higher copper prices due to demand massively outpacing supply being already a foregone conclusion.

The only thing that’s safe is that supply will grow by c. 20% – what if demand disappoints?

There a good reasons for this currently unpopular thesis.

By becoming a Premium or Premium PLUS Member, you get instant access to all my already published research reports as well as several updates.

Likewise, you qualify for eight, respectively three more exclusive reports with my best investment ideas plus updates on the featured businesses over the next twelve months.

Premium PLUS Members also get access to all Premium publications.